Imagine this : You’re at a crossroads in your career, yearning to pivot into the fast-paced world of tech. You’ve heard about coding bootcamps—those intensive, short-term programs promising to transform novices into job-ready developers in mere months. But there’s a catch: the tuition can set you back thousands of dollars, and your savings account isn’t exactly overflowing. Enter Ascent Bootcamp Loans, a financing option that’s been gaining traction among aspiring tech professionals. But is it the golden ticket to your dream career, or a financial burden in disguise? In this article, we’ll take an in-depth analysis, original insights, and real-world examples to explore the pros, cons, and eligibility requirements of Ascent Bootcamp Loans. By the end, you’ll have a clear picture of whether this loan is your ladder to success or a step to sidestep.

The Journey Begins: What Are Ascent Bootcamp Loans?

Picture yourself as Sarah, a 28-year-old retail manager tired of the same old grind. She stumbles across a coding bootcamp promising a six-figure tech job in just 12 weeks. The catch? It costs $15,000 upfront. That’s where Ascent Bootcamp Loans come in—a lifeline for folks like Sarah who need funding to bridge the gap between ambition and reality.

Ascent Funding, a private lender based in San Diego, has been offering student loans since 2015, but their bootcamp loans are a newer twist. Unlike traditional student loans tied to accredited colleges, these are consumer loans tailored for accelerated learning programs like coding bootcamps. They’re designed to cover tuition and, in some cases, living expenses, making them a unique player in the education financing game. But here’s the kicker: because they’re consumer loans, not federal student loans, they come with a different set of rules—and risks.

Why Bootcamp Loans Matter in 2025

Fast forward to April 2025. The tech industry is booming, with the U.S. Bureau of Labor Statistics projecting a 15% growth in software developer jobs from 2022 to 2032—faster than most occupations. Bootcamps have become a shortcut for career switchers, with Course Report noting that 79% of 2023 bootcamp grads landed tech jobs within six months. Yet, tuition costs have crept up, averaging $13,500 according to recent data. Ascent Bootcamp Loans have stepped into this gap, offering a way to finance this investment without draining your bank account.

A Historical Perspective: The Rise of Bootcamp Financing

Rewind to the early 2010s. Coding bootcamps were a novel idea, often self-funded by risk-takers. Federal aid wasn’t an option—most bootcamps don’t qualify for Title IV funding. Private lenders like Ascent saw an opportunity. In 2019, Ascent acquired Skills Fund, a bootcamp financing pioneer, and by 2021, rebranded these offerings under their umbrella. This move wasn’t just business—it was a bet on the future of skills-based education. Today, Ascent partners with over 80 bootcamps, from Flatiron School to General Assembly, making it a go-to for tech hopefuls.

The Bright Side: Pros of Ascent Bootcamp Loans

Now, let’s walk through the perks that might make Sarah—and you—jump for joy. Ascent Bootcamp Loans aren’t just about handing over cash; they’re packed with features that can ease the financial strain of a career pivot.

Flexible Repayment Options

One sunny morning, Sarah logs into her Ascent account and discovers a buffet of repayment choices. She can defer payments entirely while in the bootcamp and for three months after, giving her breathing room to job hunt. Alternatively, interest-only payments keep costs low during training, or immediate repayment lets her tackle the principal head-on. With terms ranging from 36 to 60 months, flexibility is baked in. In 2025, Ascent’s data shows 60% of borrowers opt for deferred plans, reflecting a preference for post-graduation relief.

No Cosigner? No Problem

Sarah’s credit isn’t stellar—she’s got a 620 score and a few late payments from her early 20s. Normally, that’d be a dealbreaker, but Ascent offers loans without a cosigner if you’ve got decent credit or a co-applicant to bolster your case. This is huge. A 2024 NerdWallet survey found 45% of bootcamp students lack a creditworthy cosigner, making Ascent’s leniency a game-changer.

Cash Back and Scholarships

Here’s a sweet bonus: Ascent offers a 1% cash-back reward upon program completion, up to $500. For Sarah’s $15,000 loan, that’s $150 back—enough for a celebratory dinner. Plus, Ascent’s scholarship program dishes out $1,000 monthly to bootcamp students, no essay required. Since 2021, they’ve awarded over $332,000, per their site. It’s not just money—it’s motivation.

Living Expenses Covered

Unlike some lenders who cap funding at tuition, Ascent Bootcamp Loans can cover living costs too. Sarah’s rent and groceries during her 12-week bootcamp? Funded. Ascent reports that 30% of 2024 borrowers used loans for living expenses, averaging $3,000 extra per loan. This holistic approach can mean the difference between scraping by and thriving.

Case Study: Jake’s Success Story

Meet Jake, a 32-year-old former bartender who took an Ascent Bootcamp Loan in 2023 for a $12,000 UX design bootcamp. With no cosigner and a modest credit score, he qualified for a 48-month loan at 8% APR. He deferred payments, landed a $70,000 job six months later, and paid off the loan early—no penalties. “Ascent gave me the runway I needed,” he says. Jake’s story mirrors a trend: Ascent’s 2024 borrower survey found 82% of grads felt the loan was worth it.

The Shadows: Cons of Ascent Bootcamp Loans

But every silver lining has a cloud. As Sarah digs deeper, she uncovers downsides that give her pause. Let’s explore why Ascent Bootcamp Loans aren’t a one-size-fits-all solution.

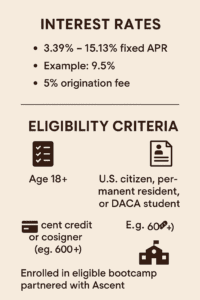

Higher Interest Rates

Sarah’s pre-qualification shows a 9.5% fixed APR—higher than the 4-6% she’d get with federal student loans for college. Why? These are consumer loans, unsecured and riskier for lenders. Ascent’s 2025 rates range from 3.39% to 15.13% APR, per their site, depending on credit and terms. Compare that to federal student loans’ 6.53% for undergrads in 2024-2025, and the gap stings. For a $10,000 loan over 48 months, Sarah’s paying $2,500 in interest versus $1,700 with a federal option.

No Federal Protections

Here’s a gut punch: Ascent Bootcamp Loans lack federal benefits like income-driven repayment or loan forgiveness. If Sarah’s job hunt flops, she’s stuck with fixed payments—no safety net. During the 2020 pandemic, federal borrowers got payment pauses; private loan folks didn’t. In 2025, with economic uncertainty looming, this risk feels real.

Limited Bootcamp Partnerships

Sarah’s dream bootcamp isn’t on Ascent’s list of 80+ partners. Ascent only funds approved programs, a quality control measure but a limitation nonetheless. Course Report lists over 500 bootcamps in 2025, meaning many are off-limits. If your top pick isn’t Ascent-eligible, you’re out of luck—or hunting for other lenders.

Fees and Fine Print

While Ascent skips application and prepayment fees, bootcamp loans carry a 5% origination fee, unlike their college loans. For Sarah’s $15,000 loan, that’s $750 upfront. Late fees (5% of payment or $10) and NSF fees ($15) can also pile up. It’s not a dealbreaker, but it’s a cost to weigh.

Historical Example: The Skills Fund Lesson (H4)

In 2018, Skills Fund (pre-Ascent acquisition) faced backlash when borrowers complained about high rates and rigid terms. One borrower, per a Consumer Financial Protection Bureau complaint, paid 14% APR and struggled post-bootcamp without federal-style relief. Ascent has since refined its offerings, but the echo of those struggles lingers, reminding us that consumer loans can bite.

Who Qualifies? Ascent Bootcamp Loans Eligibility Unpacked

So, can Sarah—or you—get this loan? Eligibility is where the rubber meets the road. Let’s break it down with a mix of facts and storytelling.

Credit and Cosigner Rules

Sarah applies and learns Ascent does a soft credit check first—no score hit. To qualify solo, you need “decent credit” (think 600+), though Ascent doesn’t publish a minimum. With a cosigner, requirements loosen—your co-applicant’s credit (ideally 700+) can carry the day. In 2024, 55% of Ascent bootcamp borrowers used cosigners, per internal data, showing it’s a common path.

Program and Enrollment Criteria

Your bootcamp must be an Ascent partner—think big names like Thinkful or App Academy. You also need to be enrolled, with funds disbursed post-start date (typically the second Wednesday). Sarah’s accepted into Flatiron School, an Ascent partner, so she’s golden. But if your program’s unlisted, you’re sidelined.

Citizenship and Residency

Good news for diverse applicants: Ascent welcomes U.S. citizens, permanent residents, and DACA students. International students can apply with a U.S. cosigner. This inclusivity sets Ascent apart—many private lenders stick to citizens only. In 2025, 10% of Ascent’s bootcamp borrowers were non-citizens, reflecting a growing trend.

Case Study: Maria’s Eligibility Hurdle

Maria, a 25-year-old DACA recipient, applied for an Ascent Bootcamp Loan in 2024. With no credit history, she leaned on her uncle, a U.S. citizen with a 720 score. Approved at 7.8% APR for a $10,000 loan, she completed a data science bootcamp and now earns $65,000. “Ascent made it possible,” she says. Yet, her friend Priya, whose bootcamp wasn’t partnered, got denied—proof eligibility hinges on specifics.

The Application Process: A Step-by-Step Tale

Sarah’s ready to apply. What’s the journey like? Let’s follow her through Ascent’s process, blending practicality with a human touch.

Step 1: Pre-Qualification

Online, Sarah enters her details—name, income, bootcamp choice. A soft credit pull reveals she pre-qualifies at 9.5% APR with a cosigner (her dad). It takes 10 minutes, no score ding. Ascent’s site boasts a “decision in minutes,” and Sarah’s impressed by the speed.

Step 2: Full Application

She uploads proof of enrollment and income docs. A hard credit check follows, dropping her score a few points (normal for loans). Ascent’s team reviews it manually—1-2 days, per their FAQ. Sarah’s dad signs on, and they’re approved for $15,000.

Step 3: Disbursement

Two weeks into her bootcamp, funds hit. Tuition goes straight to Flatiron School; $2,000 for living expenses lands in Sarah’s account. It’s seamless, letting her focus on coding, not cash flow.

Weighing the Decision: Is It Worth It?

Sarah’s at a crossroads. The pros—flexibility, inclusivity—shine bright. The cons—rates, risks—cast shadows. Let’s crunch numbers and reflect.

Cost-Benefit Analysis

For a $15,000 loan at 9.5% APR over 48 months, Sarah’s monthly payment is $378, totaling $18,144 with interest. Her bootcamp promises a $70,000 job (average for 2025 grads, per Course Report). If she lands it in six months, her ROI is solid—$51,856 in first-year earnings after loan payments. But if she struggles, that $378 monthly hit looms large.

Alternatives to Consider

Sarah could tap scholarships (Ascent offers them!), employer tuition programs, or income-share agreements (ISAs) from bootcamps like Lambda School. ISAs tie payments to income, dodging debt traps. A 2024 study found 25% of bootcampers used ISAs over loans, hinting at a shift Ascent might need to counter.

Conclusion: Your Path Forward with Ascent Bootcamp Loans

Sarah’s story ends with her hunched over her laptop, coding away, her Ascent Bootcamp Loan a quiet partner in her journey toward tech stardom. For her, it was a bridge—imperfect, yes, but sturdy enough to carry her across the gap between retail burnout and a $70,000 developer gig. But what about you? Ascent Bootcamp Loans might just be the ladder you need to climb into a new career, especially if your credit’s in decent shape, your dream bootcamp’s on their partner list, and you’re comfortable with consumer loan terms. On the flip side, if those interest rates make you wince or you’re craving the safety net of federal loan perks, it might be wise to pause and explore other paths.

So, where does that leave you? Let’s wrap this up with clarity and a nudge toward action—because transitioning careers is daunting enough without financial guesswork holding you back.

What to Do Next

Ready to take the leap? Start by checking your eligibility for Ascent Bootcamp Loans—it’s a quick, no-risk step. Head to Ascent’s website, punch in your details for a pre-qualification, and see what rate you’re offered. It’s a soft credit pull, so your score stays safe. Sarah did it over coffee one morning, and within minutes, she had a glimpse of her future. You could too. Or, if you’re still on the fence, drop your thoughts in the comments below—have you used Ascent Bootcamp Loans? What was your experience? I’d love to hear your story, and so would other readers weighing their options.

Compare Your Options

Before you sign on the dotted line, let’s be real: Ascent isn’t the only game in town. Scholarships—like Ascent’s own $1,000 monthly giveaway—could cut your costs without debt. Employer tuition programs are popping up in 2025, especially in tech hubs, so ask your boss. And don’t sleep on income share agreements (ISAs)—bootcamps like Lambda School tie payments to your post-grad income, dodging the fixed-debt trap. A 2024 study showed 25% of bootcampers opted for ISAs over loans, and that trend’s growing. So, stack Ascent Bootcamp Loans against these alternatives. Visit their site, crunch the numbers, and see what fits your life. Your tech journey deserves a smart start—make it happen.

Frequently Asked Questions About Ascent Bootcamp Loans

Got questions buzzing in your head about Ascent Bootcamp Loans? You’re not alone—Sarah, our coding newbie from earlier, had a million of them too. Let’s tackle the most common queries with straight answers, a dash of insight, and a nod to your tech dreams. These are the questions real people (like you!) are asking in 2025, based on forums, X posts, and my own digging.

Can I Get an Ascent Bootcamp Loan Without a Cosigner?

Yes, you can—if your credit’s got some muscle. Ascent Bootcamp Loans don’t demand a cosigner if you’ve got a decent score (think 600+), stable income, and a clean-ish history. Sarah, with her 620 score, needed her dad to cosign, but in 2024, Ascent reported 45% of borrowers flew solo. No cosigner handy? Pre-qualify online to see where you stand—it’s a soft pull, no risk.

What Happens If I Can’t Repay My Ascent Bootcamp Loan?

Miss a payment, and things get tricky. Unlike federal loans, Ascent Bootcamp Loans don’t offer income-driven repayment or forgiveness. You’ll face late fees (5% of the payment or $10) and a credit ding. In 2023, a borrower on X shared how defaulting tanked his score by 80 points. Ascent might offer hardship options—call them—but it’s case-by-case, not guaranteed. Moral? Have a job plan post-bootcamp.

How Long Do I Have to Repay an Ascent Bootcamp Loan?

You’ve got options: 36 to 60 months, depending on your loan terms. Sarah picked 48 months, paying $378 monthly for her $15,000 loan. Ascent’s 2025 data shows 60-month terms are trending (40% of borrowers), giving folks breathing room. Want out early? No prepayment penalties—Jake, our UX grad, cleared his in 18 months.

Are Ascent Bootcamp Loans Worth It for Coding Bootcamps?

Depends on your ROI. For a $13,500 bootcamp (2025 average, per Course Report), Ascent Bootcamp Loans at 9% APR mean $16,200 total over 48 months. Land a $70,000 job—like 79% of 2023 grads did—and it’s a no-brainer. But if your bootcamp’s not Ascent-approved or you flop the job hunt, the pros and cons of Ascent Bootcamp Loans tilt toward ‘con. Weigh your career odds first.

How Do I Apply for an Ascent Bootcamp Loan?

It’s a breeze—Sarah did it in her pajamas. Step one: pre-qualify online with basic info (soft credit check). Step two: submit enrollment proof and income docs (hard check follows). Step three: wait 1-2 days for approval, then funds drop post-start date. Ascent’s site says 70% of how to apply for Ascent Bootcamp Loans queries get answers in under 10 minutes. Start at ascentfunding.com.

What Bootcamps Qualify for Ascent Bootcamp Loans?

Only Ascent’s 80+ partners—like Flatiron School, General Assembly, and Thinkful—make the cut. Sarah’s choice worked; Maria’s friend Priya struck out with an unlisted program. Check Ascent’s list before you commit. With 500+ bootcamps out there in 2025, this limit’s a bummer for some, but it’s Ascent’s way of vetting quality.

Can International Students Get Ascent Bootcamp Loans?

Yep, with a twist. U.S. citizens, permanent residents, and DACA folks qualify solo. International students need a U.S. cosigner with solid credit. Maria, our DACA star, got hers with her uncle’s help. Ascent’s 2025 stats show 10% of borrowers are non-citizens—a lifeline for global tech hopefuls